Key Takeaways

- Your Initial Enrollment Period (IEP) is a 7-month window centered on your 65th birthday — enrolling in the first 3 months guarantees coverage starts on your birthday month.

- Start researching Medicare Supplement and Part D plans at least 3 months before turning 65, so you can enroll the day your coverage begins.

- Missing key deadlines can trigger permanent late enrollment penalties for Part B (10% per year delayed) and Part D (1% per month delayed).

- Your 6-month Medigap Open Enrollment Period starts automatically when Part B begins — this is your one guaranteed-issue window for supplement coverage.

Turning 65 is a milestone that comes with a long list of Medicare decisions, and each one has its own deadline. Miss a window by even a few weeks, and you could face permanent penalties, coverage gaps, or limited plan choices that follow you for the rest of your time on Medicare.

The problem is not that the information is unavailable. It is that Medicare's enrollment rules are scattered across dozens of government pages, and no one hands you a single, clear calendar. That is what this article provides: a month-by-month timeline that tells you exactly what to do and when, starting a full year before your 65th birthday and continuing through your first year of coverage.

Whether you are planning ahead or already inside your enrollment window, use this timeline to stay on track and avoid costly mistakes.

Why a Medicare Timeline Matters

Medicare is not a single decision. It is a sequence of interconnected choices — Part A, Part B, Part D, supplemental coverage — each with its own enrollment window and penalty structure. Getting one step wrong can cascade into problems that are expensive or impossible to undo.

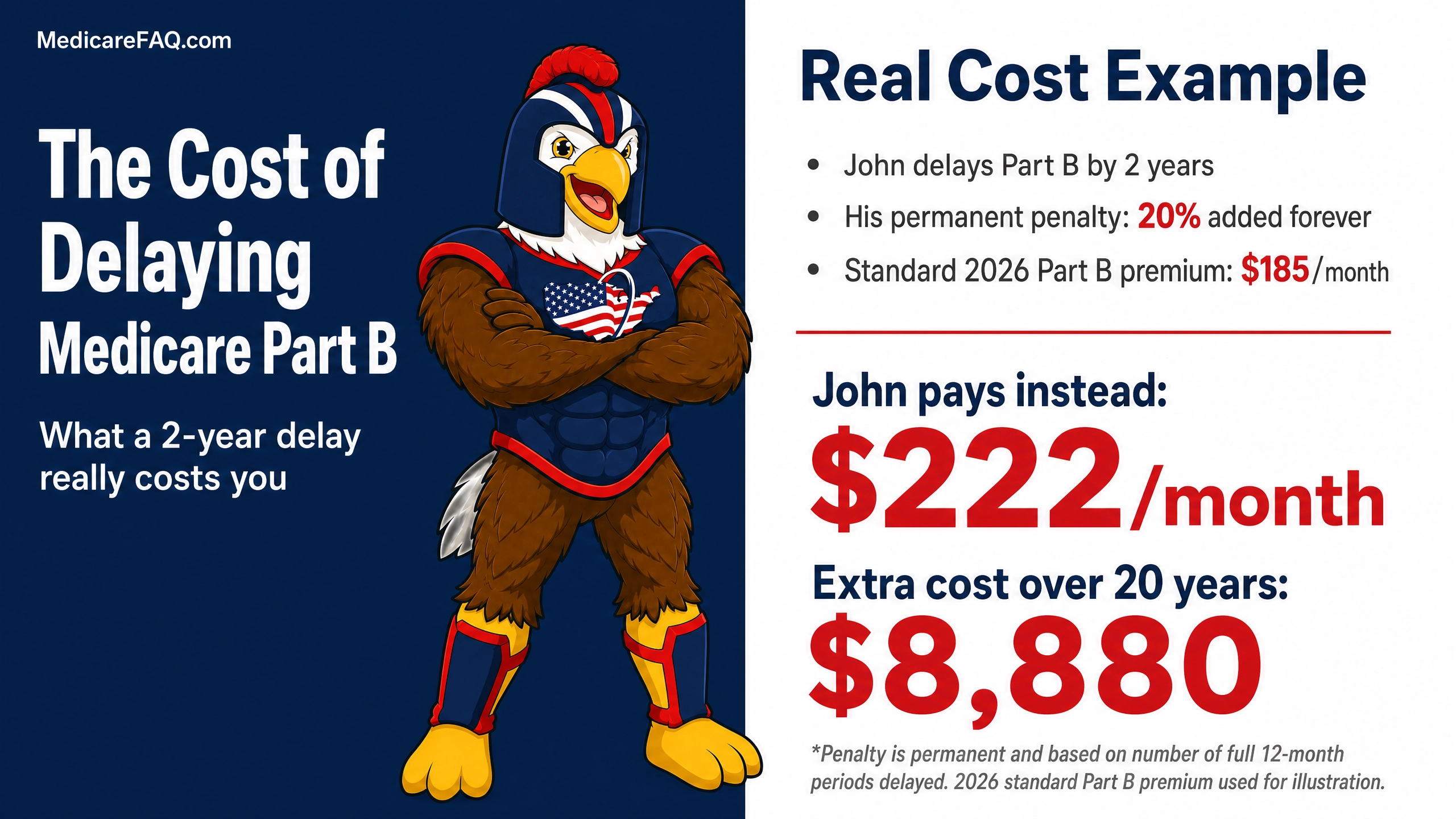

For example, delaying Part B enrollment without qualifying employer coverage triggers a late enrollment penalty of 10% for every 12-month period you could have had Part B but did not. That penalty is permanent — it never goes away. Similarly, going 63 or more consecutive days without creditable drug coverage triggers a Part D penalty that compounds every month you were uncovered.

A clear timeline eliminates the guesswork. When you know what is coming three, six, or twelve months ahead, you can research your options without pressure, gather the documents you need, and enroll at the optimal moment for the earliest possible coverage start date.

12 Months Before You Turn 65: Research and Preparation

This is your planning phase. No enrollment actions are required yet, but the research you do now will save you significant stress later. Start by understanding the basic structure of Medicare — what Parts A through D cover, how they work together, and where the gaps are.

At this stage, your primary tasks are:

Learn the four parts of Medicare. Part A covers hospital stays, Part B covers outpatient and doctor services, Part D covers prescription drugs, and Part C (Medicare Advantage) is an alternative delivery system that bundles A, B, and often D into one plan. Our Medicare Parts A, B, C, and D explained simply guide breaks this down clearly.

Decide between Original Medicare + Medigap vs. Medicare Advantage. This is the biggest structural decision you will make. Comparing Medicare Supplement vs. Medicare Advantage side by side helps you understand the tradeoffs in cost, flexibility, and provider access.

Review your current medications. Make a complete list of every prescription you take, including dosage and pharmacy. You will need this when comparing Part D plans later.

Check your Social Security status. If you are already receiving Social Security benefits, you will be enrolled in Parts A and B automatically. If not, you will need to sign up manually.

Understand your employer coverage situation. If you or your spouse have active employer coverage from a company with 20+ employees, you may be able to delay Part B without penalty. Read our guide on how Medicare works with employer health plans to understand your options.

Set a Calendar Reminder

Mark the date exactly 3 months before your 65th birthday. That is when your Initial Enrollment Period opens and when you should be ready to act. Everything you do in this 12-month planning phase prepares you for that moment.

6 Months Before Your Birthday: Narrow Your Choices

With six months to go, shift from general research to specific plan comparison. By now you should understand the Medicare landscape well enough to focus on the decisions that apply to your situation.

If you are choosing Original Medicare + Medigap: Begin comparing Medicare Supplement plans in your area. Since Medigap benefits are standardized by letter (Plan G from one insurer covers the same things as Plan G from another), your comparison is primarily about price, carrier stability, and pricing method. Our guide to finding your best Medigap plan walks through this process in detail.

If you are leaning toward Medicare Advantage: Start reviewing plans available in your zip code. Pay attention to provider networks, drug formularies, prior authorization requirements, and maximum out-of-pocket limits. The key questions to ask when comparing Medicare Advantage plans will help you evaluate each option critically.

For everyone: Begin comparing Part D prescription drug plans using your medication list. Part D plans vary significantly in which drugs they cover, what tier they place them on, and which pharmacies are preferred. Even a small formulary difference can mean hundreds of dollars per year.

This is also the time to gather documents you will need for enrollment: your Social Security number, proof of citizenship or legal residency, current insurance information, and employment history if you plan to claim a Special Enrollment Period later.

3 Months Before Your Birthday: Your IEP Opens

Your Initial Enrollment Period officially begins three months before the month you turn 65. This is the most important enrollment window in your entire Medicare journey. Enrolling during these first three months guarantees your coverage starts on the first day of your birthday month — the earliest possible start date.

Here is what to do during this critical window:

Enroll in Medicare Parts A and B. If you are not automatically enrolled (because you are not yet collecting Social Security), apply online at SSA.gov, by phone at 1-800-772-1213, or at your local Social Security office. The online application takes 10–30 minutes.

Confirm your Part B start date. If you enroll during the first three months of your IEP, Part B starts the first day of your birthday month. If you enroll during your birthday month or later, coverage is delayed by 1–3 months.

Enroll in a Part D plan (if choosing Original Medicare). Your Part D coverage can begin the same day as your Part B. Choose the plan that best covers your specific medications at your preferred pharmacy.

Apply for your Medigap plan (if choosing Original Medicare + supplement). Your Medigap Open Enrollment Period starts the month your Part B begins. Apply during this window for guaranteed acceptance regardless of health history. Plan G is the most popular choice for new beneficiaries in 2026.

Or enroll in Medicare Advantage (if choosing that path instead). MA plans replace Original Medicare, so you would not also enroll in a standalone Part D or Medigap plan.

Do Not Wait Until Your Birthday Month

Enrolling in the first three months of your IEP gives you the earliest coverage start date. Waiting until your birthday month or later delays when your coverage begins and compresses the time you have to set up supplemental coverage. There is no advantage to waiting.

Your Birthday Month: Coverage Begins

If you enrolled during the first three months of your IEP, your Medicare Part A and Part B coverage starts on the first day of this month. This is also when your 6-month Medigap Open Enrollment Period officially begins.

During your birthday month, confirm the following:

Your Medicare card has arrived. It typically arrives 2–3 months before your coverage start date. If it has not arrived, contact Social Security at 1-800-772-1213.

Your Part D plan is active. Check that your pharmacy has your new Part D information on file so prescriptions process correctly from day one.

Your Medigap plan is in force. If you applied for a Medicare Supplement plan, confirm your policy start date aligns with your Part B effective date. There should be no gap between when your old coverage ends and Medicare begins.

Notify your previous insurer. If you are leaving employer coverage, COBRA, or marketplace insurance, formally cancel that plan effective the day before your Medicare starts to avoid paying double premiums.

This is also a good time to read 5 things to do after you receive your Medicare card for a complete post-enrollment checklist.

1–3 Months After Your Birthday: Final IEP Window

Your Initial Enrollment Period extends three months past your birthday month. If you have not yet enrolled in Part B, you still can — but coverage will be delayed. Enrolling in the month after your birthday means coverage starts two months later. Enrolling two months after means a three-month delay.

| When You Enroll | Part B Coverage Starts |

|---|---|

| 3 months before birthday month | 1st day of birthday month |

| 2 months before birthday month | 1st day of birthday month |

| 1 month before birthday month | 1st day of birthday month |

| During birthday month | 1 month after enrollment |

| 1 month after birthday month | 2 months after enrollment |

| 2 months after birthday month | 3 months after enrollment |

| 3 months after birthday month | 3 months after enrollment |

As the table shows, there is a clear incentive to enroll early. Every month you delay past the first three months of your IEP pushes your coverage start date further out — and leaves you potentially uninsured during the gap.

If you are in this window and have not yet enrolled, do so immediately. You can still avoid late penalties as long as you complete enrollment before your IEP closes. But once it closes, your next opportunity is the General Enrollment Period (January 1–March 31), with coverage not starting until July 1 — plus a permanent penalty.

Your First Year of Coverage: What to Monitor

Once your Medicare coverage is active, the urgency drops — but there are still important dates and decisions to track during your first year.

Months 1–6 (Medigap Open Enrollment): Your guaranteed-issue window for Medicare Supplement plans lasts six full months from your Part B start date. If you have not yet enrolled in a Medigap plan and want one, this window is closing. After it ends, insurers in most states can deny you or charge higher premiums based on pre-existing conditions.

October 15 – December 7 (Annual Enrollment Period): This is when you can switch Medicare Advantage plans, change Part D plans, or move between Original Medicare and Medicare Advantage. Even in your first year, it is worth reviewing whether your Part D plan still covers your medications at the best price. Our guide on avoiding common enrollment mistakes covers what to watch for.

January 1 – March 31 (Medicare Advantage Open Enrollment): If you enrolled in a Medicare Advantage plan and are unhappy with it, this period allows you to switch to a different MA plan or drop back to Original Medicare and pick up a Part D plan. Note that switching from Medicare Advantage to Original Medicare may require medical underwriting for Medigap in most states.

Track your spending. Review your Medicare Summary Notices quarterly to catch billing errors, confirm your plan is covering services correctly, and keep records for tax purposes. Understanding your total Medicare costs helps you budget accurately for the year ahead.

What If You're Still Working at 65?

Not everyone retires at 65, and Medicare's rules accommodate that — but only under specific conditions. If you are still working and have health insurance through your employer (or your spouse's employer), you may be able to delay Medicare Part B without penalty. The key requirement: the employer must have 20 or more employees.

If your employer has 20+ employees, your group health plan is considered "primary" and pays first. Medicare becomes secondary. In this situation, you can safely delay Part B and enroll later through a Special Enrollment Period when the employment or coverage ends — with no late penalty.

However, there are critical nuances:

COBRA does not count. COBRA continuation coverage is not considered active employer coverage. If you retire and elect COBRA, your Part B penalty clock starts ticking immediately. Read more about COBRA and Medicare coverage differences.

Retiree insurance does not count. Retiree health benefits from a former employer do not qualify you for a Special Enrollment Period.

Small employers (fewer than 20 employees): Medicare becomes primary even if you have employer coverage. You should enroll in Part B during your IEP to avoid penalties.

HSA considerations: Once you enroll in any part of Medicare, you can no longer contribute to a Health Savings Account. If you have an HSA, plan your Medicare enrollment timing carefully. Our article on Medicare and HSA rules explains the details.

Part A is usually free. Most people should enroll in Part A at 65 even if they delay Part B, since Part A is premium-free for those with 40+ quarters of work history. The exception is if enrolling in Part A would affect your HSA contributions.

When your employment ends (or you lose employer coverage), you have an 8-month Special Enrollment Period to sign up for Part B. Do not wait until the end of this window — enroll promptly so your coverage starts sooner and you can begin your Medigap Open Enrollment Period.

Medicare Timeline FAQ

Your Next Steps

Medicare enrollment is not something you figure out in an afternoon. It is a process that rewards preparation. The earlier you start — ideally 12 months before your 65th birthday — the more confident and informed your decisions will be.

Here is your action plan based on where you are right now:

More than 6 months out? Start with our Medicare 101 guide and the New to Medicare checklist to build your foundation.

3–6 months out? Compare your supplemental coverage options. If leaning toward Medigap, read our best Medigap plan guide. If considering Advantage, review Medicare Advantage plans in your area.

Inside your IEP right now? Enroll in Parts A and B immediately if you have not already. Then choose your Part D and supplemental coverage before your birthday month.

Just turned 65? Confirm your coverage is active, check that your prescriptions are processing, and remember your Medigap Open Enrollment window is counting down.

If you want personalized guidance, speaking with a licensed Medicare specialist can help you navigate the specifics of your situation — your medications, your doctors, your budget, and your state's rules. The decisions you make now set the foundation for your healthcare costs for years to come, and getting them right the first time is far easier than trying to fix them later.

Related Articles

Have Medicare questions?

Our licensed Medicare agents are available to help you find the right coverage.